The Art & Science of Company Valuations

Welcome back to the Mid Market Insider!

Let’s jump in…

This week I want to educate you on how to accurately value your business.

In this edition, we will explore:

The 3-4 key methodologies used to evaluate a company.

I'll also explain the key factors that can impact both your company's valuation and your ability to sell your business.

Some of these factors can significantly increase or decrease not only how much your company is worth, but also whether potential buyers will be interested in purchasing it at all.

Now I’ll have to break this up into a series of editions. (For your sake)

Enough of me rambling let’s get started.

There are 3 or 4 key methodologies used to evaluate a company.

1. Sum of the assets

This one is pretty straightforward. Identify the assets of the company, determine a fair market value for each, and then sum them up.

In my experience, this is rare but still used in certain situations.

2. Discounted cash flow

To calculate business value using this method, the first step is to project future cash flows. The next step would be to discount those with the appropriate cost of capital. The final result is the value of the company.

Now a lot is going on here from:

- Growth rates

- EBITDA margins

- What capital structure to use

- Calculating the after-tax cost of capital

- How much-working capital is required

While PE firms forecast cashflows, they typically do this to determine what their expected return will be, not the appropriate price to pay.

3. Multiple of EBITDA - Precedent transactions & public company comps

I am not going to go into the mechanics of EBITDA or why it is used but calculating a business’s value as a multiple of EBITDA is very common.

In order to figure out what the appropriate multiple to use is, two methods stand out:

Precedent transactions - identify similar transactions based on size, industry, geography, etc. Use those numbers to estimate a fair multiple or range of multiples.

Public company comps - identify publicly traded companies in the same industry and calculate the average EBITDA multiples those businesses are trading for.

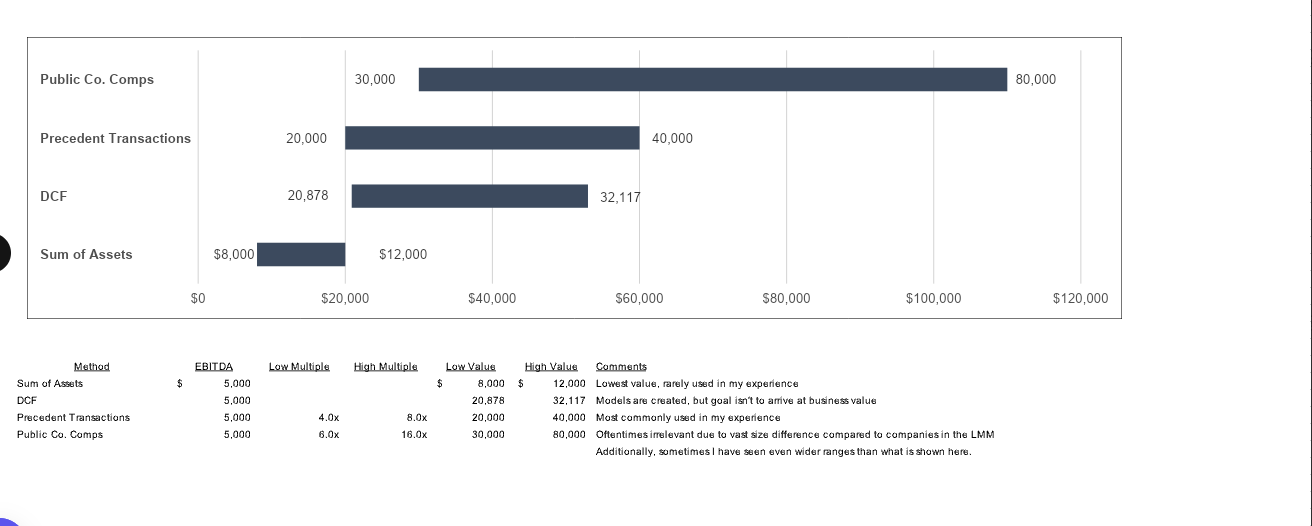

Investment bankers will use all of these methods and summarize the results on what’s called a football field.

Here’s an example:

Now specifically in the lower middle market, PE firms are going to almost exclusively look at transactions of comparably sized companies in comparably sized industries.

Now let’s move on and explore the factors that may increase or decrease the multiple.

Typically the two largest factors are:

1. Size

2. Industry

After you have a starting point there are several other factors that might have a minor effect and others which will have a larger impact.

1. Customer Concentration

(How concentrated your revenue is across your client base)

I can't overstate how harmful it can be for a company to have over 30-40% customer concentration. Some buyers won’t even consider the deal if customer concentration is high. If they do, you can expect to get a fraction of what would be paid for a company without that level of concentration.

The best method to increase the value and likelihood of selling your business is to address the customer concentration issue, if there is one.

2. Amount of Capex

(Money spent by a company to acquire, maintain or improve long-term assets)

A great example here is the asset-heavy trucking industry.

If you are replacing trucks every 5 years, your EBITDA maybe $5 million. But your annual capex to refurbish the trucks may be $2-3 million dollars.

This will have a huge impact on your valuation.

3. Macroeconomic cyclicality

(A business’s sensitivity to the macroeconomic conditions)

A great example would be construction companies. Construction companies are very profitable businesses. However, there are a lot of ups and downs in this industry.

Too much potential variability in revenue and earnings will impact the valuation negatively due to its volatile nature.

4. Project-based revenues

Another reason why construction companies are exposed to cyclicality is all their revenue is project-based.

Each year they have to rebuild their business.

5. EBITDA margins

Generally speaking people like to see 15% or higher in terms of EBITDA margins.

If you are getting above 30% then even better but above 50% then that looks suspicious.

6. Perceived Growth Potential

If you are in an industry or sector that can demonstrate some evidence that there will be growth, it will positively impact your valuation.

However, the burden of proof is on you. What I mean by this is, for example, if you land a new contract or if there is an event in the world that could drastically and positively impact the fortune of your business.

However, in any valuation you get for your business there is an assumption there is growth potential in your business but if they feel the growth potential is too small then it will, in fact, have a negative impact on your valuation.

I know that was a lot but if you want to learn more make sure to check out my YouTube video here.

The Lessons:

Valuation methods differ, but EBITDA multiples are king in the lower middle market. While there are several ways to value a company, PE firms typically focus on comparable transactions and EBITDA multiples as their go-to method.

Customer concentration can make or break your valuation. Having more than 50% of your revenue tied to a single customer could slash your company's value in half or even make it unsellable. Diversifying your customer base should be a top priority.

Context is everything. Your industry, size, growth potential, and even how your business model differs from industry norms can significantly impact your valuation. The key is understanding where you stand on these factors and working to improve them where possible.

📅 Next Week:

In next week's newsletter, we will explore why people hate Private Equity.

Keep building,

Nick

P.S.

If you want to hear more from ‘The Most Boring Guy In Private Equity’, follow me on LinkedIn and YouTube. I dive into the world of private equity, share some tips and tricks for small business owners, and most importantly, share my industry knowledge.

Make sure to follow me so you don’t miss out!

If you want to discuss your business goals in greater detail book a discovery call: https://calendly.com/nickmclean/discovery-call.

Just remember, this won’t cost you a dime and you get what you pay for :)

I just launched a podcast, Ambition with Nick!

Links can be found here:

Apple

LinkedIn: Nick McLean

Youtube: NickFourPillars